Proposal for a national pool for those who receive expensive cell and gene therapy

January 16, 2024

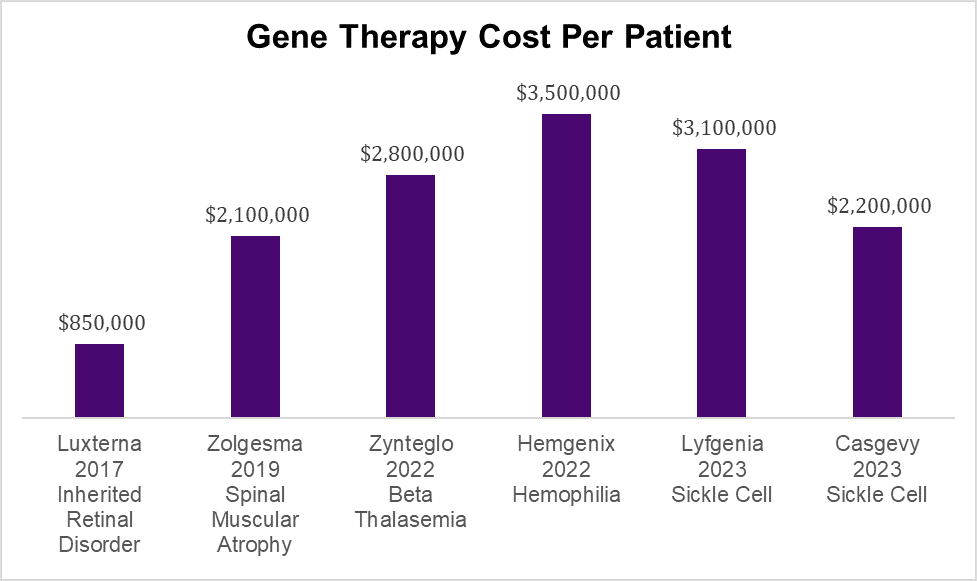

Cost of pharmaceutical only; cost of administration and hospitalization if necessary are separate. Source: Various news outlets

Recent news that gene therapy can cure sickle cell disease, hemophilia, thalassemia, spinal muscular atrophy and other dreaded diseases is wonderful news for humanity, but creates a giant challenge for employer sponsored health insurance. Most employers don’t have nearly the size population of employees and family members to be able to absorb the shock of such large costs without causing large premium increases. In some instances, the costs of these treatments could even threaten company viability. Many employers purchase reinsurance to decrease this risk of volatility, but this is expensive, and some reinsurers “laser out” members with known diseases.

An op ed in Health Affairs Forefront this week proposes Medicare Part E, to provide coverage for the expensive pharmaceuticals needed for treatment of rare diseases. The benefit would be funded by taxes and would pool together those who needed the expensive treatment across all different types of health care finance, including employer sponsored health insurance, marketplace plans, Medicare, and Medicaid.

There are a lot of good elements to this plan. It makes actuarial sense to have the largest possible risk pool for treatments that are rare and expensive, and the pandemic showed us that the government can acquire expensive drugs for a lower price. Government administrative costs would also likely be lower than commercial reinsurance which must include a risk premium and profit. The proposal to create Medicare Part E is consistent with the government approach of offering coverage for groups that are otherwise “uninsurable,” such as the elderly, the poor, the disabled and those with end stage renal disease (Medicare), and the poor and children (Medicaid and CHIP). Longer-term benefits from these expensive therapies will offer less advantage to companies with shorter employee tenure Removing the highest cost patients from employer sponsored health insurance would make these plans more stable, and lower health care costs could help make US companies more competitive.

There are significant barriers to implementing this proposal, which would require Congressional and executive actions. This would also require a funding source, and new taxes are never popular. Insurance companies could oppose such government intervention, and pharmaceutical companies would worry that their reimbursements would decline.

Implications for employers:

High potential reimbursement for rare disease treatment has helped drive innovation and made available new treatments for previously untreatable diseases.

This proposal puts a spotlight on the increased volatility faced by employers due to exceptionally high-cost interventions.

Employers can continue to evaluate reinsurance options, including those offered by carriers and pharmacy benefit managers. Pooling the risk of these expensive treatments for rare diseases among many employers through captives or other mechanisms can decrease volatility.

Wednesday: Hearing aid use associated with lower death rates

Thanks for reading. You can find previous posts in the Employer Coverage archive

Please “like” and suggest this newsletter to friends and colleagues. Thanks!

I've been a big proponent of this idea for several years. The idea that life saving new and wildly expensive technologies that benefits a small population of people is exactly paralleled by existing Medicare coverage of dialysis for ESRD and is best funded by spreading the cost and risk over the entire US population. Individual employers and even most health plans will struggle to pay for these therapies as well as justify the in year cost vs the lifetime quality of life and cost benefits that are likely to accrue to society but not the entity that is footing the bill.

Curing sickle cell, cystic fibrosis and the array of other lethal genetic diseases was unthinkable when I was in medical training and now that several of these are here and more will come to market over the next few years is an amazing advance.

Thank you for sharing this rationale on how these high-cost pharmaceuticals will affect the actuarial tables of insurance products! Very relevant to current work going on abroad on how national health insurance programs are struggling to create financing mechanisms to fund these much needed, yet prohibitively expensive treatments.