Shorts: US life expectancy, underinsurance, cervical screening, premiums and issues still before Congress

December 19, 2024

1. U.S. life expectancy projected to stagnate

Researchers from the Institute for Health Metrics Evaluation developed projections on how life expectancy will change in the U.S. over the next quarter century. They predict that life expectancy will increase only modestly, and U.S. life expectancy gains will lag behind other countries, so that life expectancy ranking will decline from 49th to 66th of the countries evaluated. They projected continued decline in deaths from heart disease and stroke, but increased deaths from kidney disease and drug use.

The researchers estimated 12.4 million deaths could be averted if the U.S. made improvements in drug use, obesity and tobacco use. Employer programs to promote smoking cessation and treat obesity and drug use disorder can play an important role in improving life expectancy and health.

2. Underinsured often don’t seek necessary medical care

The Commonwealth Fund reported late last month that 23% of those who were insured all year in 2023 were underinsured, meaning that they had out of pocket costs over 10% of household income (of 5% if they had income under 200% of the federal poverty level) or if their deductible was over 5% of household income. About two-thirds (66%) of those who were underinsured were on employer-sponsored health insurance plans.

Fifty-seven percent of those who were underinsured reported access problems during the year that led them to not fill prescriptions or to skip tests, treatment, or medical visits. Employers can evaluate the impact of their health insurance plan design on employee financial security. About one-quarter (27%) of employers reported in the 2024 WTW Best Practices in Healthcare Survey that they structure payroll contributions to reduce costs for targeted groups like low wage employees or certain job classes. Here’s a link to a 2019 Harvard Business Review article I co-authored about making health care affordable for low wage workers.

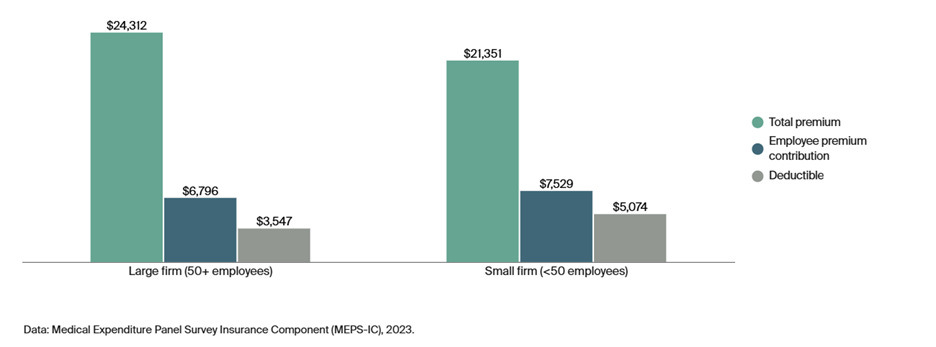

3. Premiums lower but out-of-pocket costs higher at smaller firms

Total costs, premiums and deductibles for family plans by employer size

Source: Kolb, et al Commonwealth Fund December 10, 2024

Researchers at the Commonwealth Fund used the 2023 Medical Expenditure Panel Survey to estimate total costs, employee premiums and deductibles for family plans, and found that while total premiums were lower for smaller employers (<50), both employee premiums and deductibles were higher. These high out-of-pocket costs can threaten financial security for employees of both large and small employers. These premiums are smaller than reported earlier this fall by KFF, which surveys employers as opposed to reviewing federal survey data.

4. New option for cervical cancer screening

The US Preventive Services Task Force just proposed a new recommendation that between ages 30 and 65 women could do a cervical self-swab to test for human papillomavirus (HPV) every five years instead of a pap smear every three years. This is a small change, as these self-swabs at this point must be performed in a provider office, and every five-year provider cervical HPV swabs were already an option for cervical cancer screening. Women can perform cervical swab tests at home in Australia, Denmark, the Netherlands and Sweden, and home testing will likely be approved in the future in the U.S. HPV vaccination prevents many cases of cervical cancer, so the number of cases of cervical cancer will likely continue to decrease. This draft recommendation will likely be finalized in 2025.

5. Health policy issues facing outgoing Congress

A new Congress starts its 2025-6 term on January 5, but the “lame duck” Congress continues to meet until the holidays, and there are several bills that could impact employer-sponsored health insurance that could be attached to a bill to continue government funding at the end of this calendar year.

These issues include:

Pharmacy benefit management regulations, which could “delink” PBM revenue from drug rebates or add additional transparency requirements. Some PBM regulation was in the continuing resolution that was scuttled last night. PBM regulations could impact existing PBM contracts.

Telehealth safe harbor, which allows high deductible health plans to waive pre-deductible cost sharing, expires at the end of 2024. Employers can check with their counsel about implications if Congress does not extend the safe harbor.

Exchange plan enhanced subsidies expire at the end of 2025. If Congress does not extend these, some employees might move from exchanges to employer-sponsored health insurance.

A bipartisan bill to require insurance companies to divest of retail or mail order pharmacies was filed this week but is unlikely to be acted upon in the brief time remaining in this Congressional session.